When you're on Medicare and need prescription drugs, understanding how generic drugs are covered under Part D can save you hundreds - even thousands - of dollars each year. Most people assume all prescriptions work the same way, but the truth is, Medicare Part D formularies are built to steer you toward generics, and knowing how that system works makes all the difference.

What Is a Medicare Part D Formulary?

A formulary is simply a list of drugs that your Medicare Part D plan covers. Every plan has one, and it’s not random. The Centers for Medicare & Medicaid Services (CMS) sets strict rules: every plan must include at least two different generic versions of each common medication type - like blood pressure pills, diabetes meds, or cholesterol drugs. This ensures you have choices, even if you’re only taking generics. These lists are split into five tiers. Generics almost always land in Tier 1 or Tier 2. Tier 1 is for the cheapest, preferred generics - often with a $0 to $15 copay for a 30-day supply. Tier 2 is for non-preferred generics, which might cost more - maybe $20 to $40, or 25-35% of the drug’s price. Brand-name drugs? They’re stuck in Tiers 3 to 5, where costs jump up dramatically.How Much Do Generics Actually Cost in 2025?

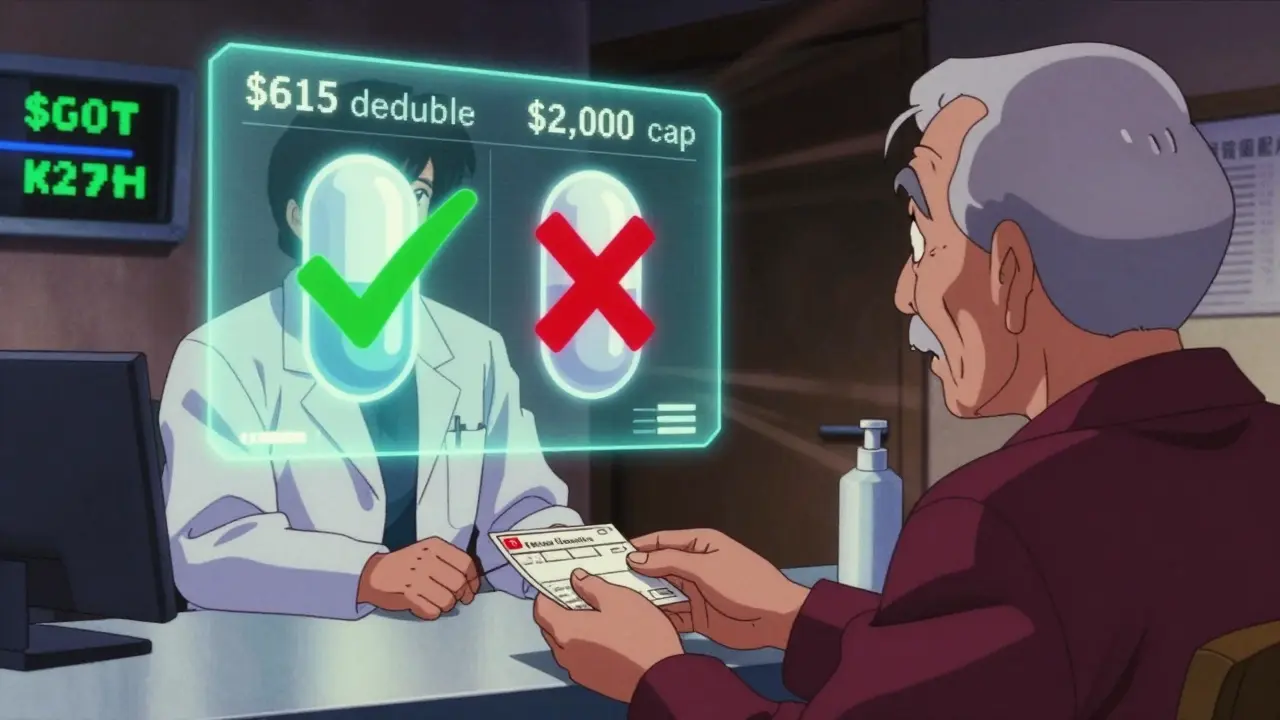

The cost structure changed big time in January 2025 thanks to the Inflation Reduction Act. Before, you hit a "donut hole" - a gap where you paid full price after spending a certain amount. That’s gone. Now, once you’ve paid $2,000 out of pocket in 2025 (rising to $2,100 in 2026), you pay nothing for any drug - generic or brand - for the rest of the year. Here’s how it breaks down:- Deductible: $615 in 2025. You pay this first, unless your plan has a $0 deductible (52% of plans do).

- Initial coverage: After the deductible, you pay 25% coinsurance on generics. The plan pays the other 75%. This continues until you hit the $2,000 out-of-pocket cap.

- Catastrophic coverage: After $2,000, you pay $0. Medicare covers nearly everything.

Why Generics Are So Much Cheaper

Generic drugs aren’t "weaker" or "inferior." They’re chemically identical to the brand-name versions. The only difference? No marketing, no patent, no R&D costs. That’s why they cost 80-85% less. In 2023, 92% of all prescriptions filled under Medicare Part D were generics. But here’s the kicker: those 92% of prescriptions made up only 18% of total drug spending. That’s because generics are so cheap. A generic statin might cost $5. A brand-name version? $150. That’s why plans push generics so hard - it saves Medicare and you money.

What If Your Generic Isn’t Covered?

This is where things get messy. Even though a drug is generic, your plan might only cover one version - say, the generic version made by Company A - and not another, even if it’s the same active ingredient. That’s called "therapeutic interchange." A lot of people get hit with surprise bills because their pharmacist tries to swap one generic for another. If the new one isn’t on your plan’s formulary, you pay full price. One Reddit user reported being charged $120 for a blood pressure generic because his plan only covered a different brand of the same drug. He had to call his plan and file a coverage request - which was approved, but not before he paid out of pocket. You can avoid this by:- Checking your plan’s formulary before enrolling - don’t just pick the cheapest plan.

- Using the Medicare Plan Finder tool and typing in every medication you take, including the exact generic name.

- Asking your pharmacist: "Is this the version my plan covers?" before they fill it.

Protected Classes and What You Can’t Be Denied

Some drug categories are protected by law. These include antidepressants, antipsychotics, anticonvulsants, immunosuppressants, antiretrovirals, and antineoplastics (cancer drugs). For these, your plan must cover every available generic version. No exceptions. That means if you’re on an antidepressant like sertraline, your plan can’t pick just one generic and deny others. You have the right to any FDA-approved version. If your plan denies coverage, you can appeal - and you’re very likely to win.How to Save More on Generics

You don’t have to just accept whatever your plan gives you. Here’s how to optimize:- Choose a $0 deductible plan. About half of Part D plans offer this. If you take even one generic a month, you skip the $615 deductible entirely.

- Use mail-order pharmacies. Many plans offer 90-day supplies at the same price as 30-day. That’s two refills for the cost of one.

- Check for manufacturer discounts. Some generic makers offer coupons - yes, even for generics. Sites like GoodRx sometimes list discounts for generic drugs too.

- Request a coverage determination. If your needed generic isn’t on your plan’s list, file a formal request. CMS data shows 83% of these requests get approved.

- Switch plans during Open Enrollment. Every fall, plans change their formularies. 37% of plans alter at least one generic’s tier. Use the Medicare Plan Finder to compare. People who switch save an average of $427 a year.

What’s Changing in 2026 and Beyond

The changes aren’t over. Starting in 2026, Medicare plans must add a "generic price comparison tool" to their member portals. That means you’ll be able to see, right on your phone, which generic version of your drug costs the least - even if it’s not the one your doctor prescribed. In 2029, Medicare will start negotiating prices for certain generic drugs. Insulin glargine (the generic version of Lantus) is already on the list. That could bring prices down even further. And there’s growing pressure to standardize formularies. Right now, one plan might cover five different generic versions of a blood pressure drug. Another might cover only one. That’s confusing and costly. The Medicare Payment Advisory Commission has recommended a national standard - and lawmakers are listening.Real Stories, Real Savings

One beneficiary in Ohio, 72, takes three daily generics: a blood pressure pill, a cholesterol med, and a thyroid drug. Before 2025, she paid $110 a month out of pocket. After hitting the $2,000 cap in July, her monthly cost dropped to $0. "I didn’t realize I was paying so much until I hit the cap," she said. "Now I don’t even think about it. I just pick up my pills." Another, a veteran in Florida, switched plans after learning his current one didn’t cover his preferred generic of metformin. He found a new plan with the same drug on Tier 1 - $0 copay. He now saves $320 a month. "I didn’t know I had a choice," he told his local senior center. "I thought I was stuck."What to Do Next

If you’re on Medicare Part D and take any generics:- Log into your plan’s website and check your formulary - specifically for every drug you take.

- Use the Medicare Plan Finder (medicare.gov/plan-compare) and enter your medications. Compare at least three plans.

- If you’re taking multiple generics, look for a plan with a $0 deductible and low Tier 1 copays.

- Call your pharmacist and ask: "Is this the version my plan covers?" before you pay.

- Mark your calendar for October - Open Enrollment starts then. Don’t wait until December.

Are all generic drugs covered under Medicare Part D?

Almost all FDA-approved generic drugs are covered, but not every version of a drug is on every plan’s formulary. Plans can choose which specific generic brands to include, even if multiple are available. For example, a plan might cover the generic version of lisinopril made by Company A but not Company B - even though both are identical. You must check your plan’s formulary to confirm coverage.

Why does my generic drug cost more than last year?

Your plan may have moved your generic to a higher tier (like from Tier 1 to Tier 2) or removed it entirely. Each fall, plans update their formularies - 37% change at least one generic’s tier placement. You’ll get an Annual Notice of Change (ANOC) in the mail. Always review it. If your drug was moved to a higher tier, you can switch plans during Open Enrollment to find one that covers it better.

Can I get my generic drug for free?

Yes - after you’ve paid $2,000 out of pocket in 2025 (rising to $2,100 in 2026), you pay $0 for all drugs, including generics, for the rest of the year. Also, many plans offer $0 copays for Tier 1 generics. If you’re on a low income, you may qualify for Extra Help, which can reduce or eliminate your monthly premiums and copays entirely.

What if my pharmacist gives me a different generic than what’s on my formulary?

Pharmacists can substitute one generic for another only if your plan allows it and your doctor hasn’t said "dispense as written." If the substitute isn’t on your plan’s formulary, you’ll pay full price. Always ask your pharmacist: "Is this the version my plan covers?" If it’s not, you can request your original drug - or file a coverage exception with your plan.

How do I know if my plan covers my generic medication?

Use the Medicare Plan Finder tool on Medicare.gov. Enter your exact drug names - including the generic version - and your zip code. The tool shows which plans cover your drugs and at what tier and cost. Don’t rely on your doctor’s recommendation alone - formularies vary by plan. Always verify before enrolling.

Comments

Rob Sims

January 22, 2026Oh wow, another article pretending Medicare is some kind of benevolent fairy godmother. Let me guess - you forgot to mention that the ‘$0 after $2,000’ only applies if you’re lucky enough to have a plan that doesn’t slap you with a $600 deductible first? And don’t even get me started on how 37% of plans change formularies every year just to screw people over mid-year. This isn’t saving money - it’s a rigged game where the house always wins, and you’re the sucker who thinks the ‘$0 copay’ is a gift.

Tatiana Bandurina

January 24, 2026The entire premise of this article is dangerously misleading. Yes, generics are cheaper - but only because the pharmaceutical companies have already extracted every dime they can from the brand-name versions first. Then they sell the same chemical to generic manufacturers who charge pennies - but only after the brand-name maker has held the market hostage for 20 years. This isn’t consumer empowerment. It’s a legal loophole dressed up as a win.

Philip House

January 25, 2026Let’s not romanticize this. The system’s still broken. The ‘$2,000 out-of-pocket cap’ sounds great until you’re 78 and on five meds, and your plan only covers one generic version of your blood pressure pill - the one that gives you dizziness. Then you’re stuck paying $120 for the version your doctor actually prescribed because the plan’s ‘preferred’ version is a chemical cousin that makes you feel like you’re being slowly drained by a vampire. And don’t get me started on how the ‘protected classes’ don’t protect you if your doctor prescribes the wrong brand name. You think you’re getting choice? You’re getting bureaucracy with a smiley face.

Jasmine Bryant

January 26, 2026Biggest tip I’ve learned: always check your plan’s formulary on Medicare.gov using the exact spelling of your generic - even if it’s just ‘metformin’ vs. ‘metformin hydrochloride’. I once got hit with a $90 bill because my plan covered ‘Metformin HCl’ but not ‘Metformin Hydrochloride’ - same thing, different paperwork. Also, mail order is a game-changer. I save $200/month just by getting 90-day supplies. And yes, GoodRx sometimes has discounts on generics - even ones you’d never think to look for. Just don’t trust your pharmacist’s word - ask for the formulary code.

shivani acharya

January 28, 2026Oh this is beautiful, isn’t it? The government says ‘you pay nothing after $2,000’ - but who’s really paying? The taxpayers. The pharmaceutical companies are laughing all the way to the bank because they just raised prices for 10 years, then let generics in as a distraction. And now you’re supposed to be grateful? Meanwhile, my cousin in India pays $2 for the same generic. Here, you need a PhD in insurance law just to get a $5 pill. And don’t even get me started on how the ‘protected classes’ are a joke - they only protect you if you’re willing to spend three months fighting with a call center that doesn’t speak English. This isn’t healthcare. It’s a psychological torture test.

Hilary Miller

January 28, 2026Switched plans last year. Saved $480. Done.

Margaret Khaemba

January 29, 2026I’m 69 and on three generics - lisinopril, atorvastatin, metformin. I used to pay $140/month. Now, after hitting the $2,000 cap in May, I pay $0. I didn’t even realize I was spending that much until I saw the statement. I didn’t know about the mail-order trick until my pharmacist mentioned it. Honestly, if you’re on meds, just spend an hour on Medicare.gov. It’s not glamorous, but it’s the only way not to get robbed. Also, write down your meds’ exact names - including the manufacturer if you know it. That’s saved me twice.

Keith Helm

January 31, 2026It is imperative to note that the Inflation Reduction Act’s provisions regarding out-of-pocket maximums are not universally applicable across all Part D plans. Certain high-deductible plans may still impose additional administrative burdens. Beneficiaries are advised to consult their plan’s Evidence of Coverage document prior to making any enrollment decisions. Furthermore, therapeutic interchange protocols remain subject to state-level pharmacy regulations, which may vary in scope and enforcement.

Daphne Mallari - Tolentino

February 1, 2026While the article presents a superficially optimistic view of Medicare Part D reforms, it conspicuously omits the systemic erosion of pharmaceutical oversight that has enabled this so-called ‘cost savings.’ The normalization of generic substitution without physician consent is a dangerous precedent - one that prioritizes fiscal efficiency over clinical nuance. One cannot help but wonder: when did healthcare become a spreadsheet exercise?

Neil Ellis

February 2, 2026Man, I used to stress about my $80 monthly pill bill. Now? I just grab my meds like I’m picking up coffee. No sweat. The $2,000 cap? That’s the real MVP. And mail-order? Best thing since sliced bread. I didn’t know I could switch plans - thought I was stuck. Turned out I was just lazy. Now I’m saving a couple hundred a year, and I actually feel like I’m not being played. It’s not perfect, but it’s a damn sight better than five years ago. Keep pushing, folks - knowledge is power.

Alec Amiri

February 2, 2026Oh wow, someone actually wrote a whole article about generics and didn’t mention Big Pharma’s secret deals with insurers? Classic. You think people are saving money? Nah. They’re just getting the cheap version while the same companies jack up the price of the brand-name ones for the 10% who still need them. And the ‘$0 after $2,000’? That’s just a bait-and-switch - you still pay $600 deductible, then 25% coinsurance, then you hit the cap… but only if you live long enough to get there. This isn’t reform. It’s a magic trick with a side of guilt.

Lana Kabulova

February 4, 2026Just a heads-up - if your plan says it covers 'metformin' but your pharmacist gives you 'metformin ER' - that’s NOT the same thing. I learned this the hard way when I ended up in the ER because my sugar crashed. The formulary listed 'metformin' - but didn’t specify immediate vs extended release. So check the exact formulation. And if your doctor didn’t write 'dispense as written' - they probably didn’t know your plan’s rules. You have to be your own advocate. Don’t trust anyone. Not the plan. Not the pharmacist. Not even your doctor. Always verify. Always. Always.

Write a comment