Quick Takeaways

- Indemnification shifts financial risk from one party (indemnitee) to another (indemnifier).

- There is a critical difference between promising to "indemnify," "defend," and "hold harmless."

- "Fundamental representations" usually have longer survival periods than "non-fundamental" ones.

- Caps and baskets are used to limit the total amount of money a party has to pay back.

The Core Difference: Indemnify, Defend, and Hold Harmless

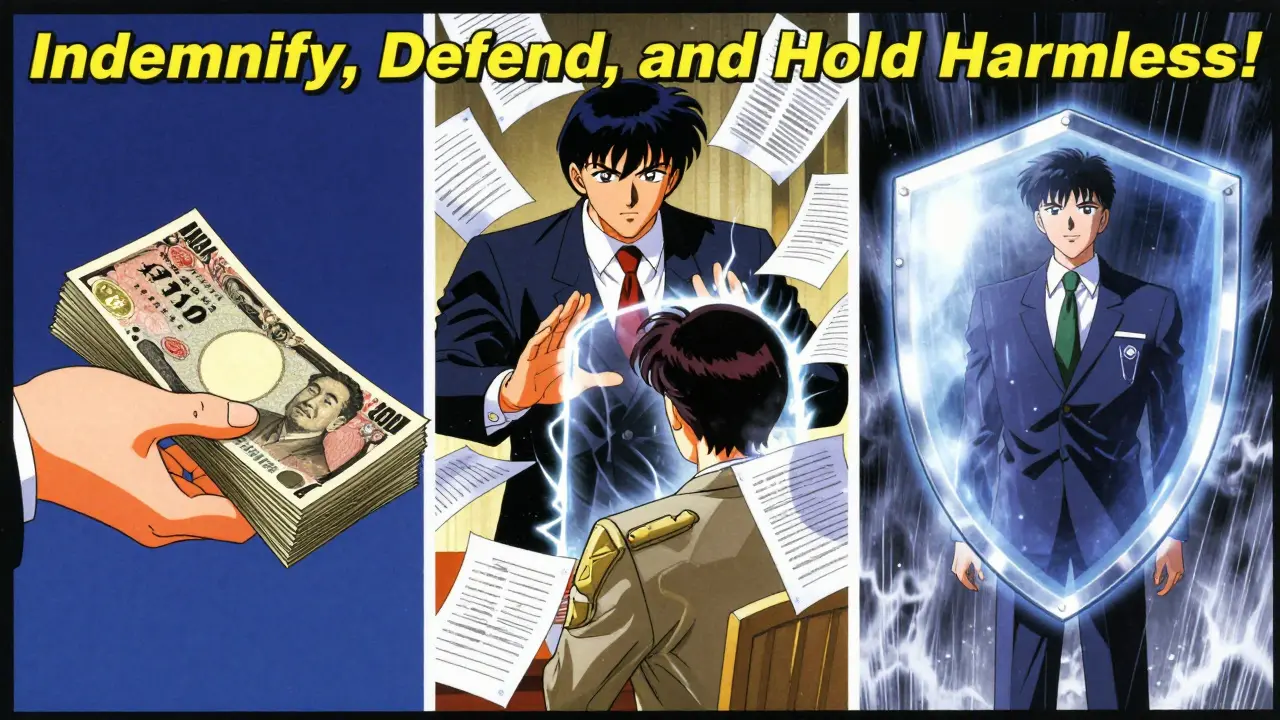

In many contracts, you'll see the phrase "indemnify, defend, and hold harmless" lumped together. While they sound similar, they actually trigger three very different obligations. If you're signing a contract, knowing these distinctions is the difference between paying a reimbursement check and paying for a high-priced law firm in real-time.Indemnify is essentially a reimbursement. If the buyer loses money because of the seller's mistake, the seller pays them back. It's a financial restoration after the loss has occurred.

Defend is more immediate. This requires the indemnifying party to pick up the legal tab from day one. They don't just pay the final judgment; they pay the hourly rates for the lawyers fighting the suit. This is often the most expensive part of the process.

Hold Harmless is a shield. It means the indemnifier agrees not to sue the other party for losses they caused. It prevents the person providing the indemnity from trying to shift the blame back to the person they are protecting.

How Indemnification Works in Practice

For a claim to be valid, a "triggering event" must happen. This isn't a vague occurrence; it's a specific action defined in the contract. For example, if a cloud service provider fails to maintain security standards and a data breach occurs, that failure is the trigger. The provider then owes the customer for the cost of notifying affected users and providing credit monitoring services.The scope of what is covered varies. Some agreements only cover "direct damages" (the actual money lost), while others might include "consequential damages" (lost profits or reputation damage). Most savvy negotiators try to exclude consequential damages because they are unpredictable and can bankrupt a small company.

| Feature | Unilateral Indemnification | Mutual Indemnification |

|---|---|---|

| Direction | One party protects the other | Both parties protect each other |

| Typical Use | High-leverage deals (e.g., Big Tech vs. Startup) | Balanced partnerships or construction contracts |

| Risk Profile | High risk for the indemnifier | Shared and balanced risk |

| Common Example | Software IP infringement claims | Workplace injury claims on a joint site |

Managing the Money: Caps, Baskets, and Survival Periods

Nobody wants to sign a "blank check." To prevent an indemnification clause from becoming a bottomless pit of liability, parties use financial guardrails.A Cap is the maximum amount one party will ever have to pay. For instance, a seller might agree to indemnify a buyer, but only up to 20% of the total purchase price of the company. Once that limit is hit, the buyer absorbs any further losses.

A Basket (or deductible) works like insurance. It's a threshold that must be met before the indemnification kicks in. If the basket is $10,000, the buyer can't claim for a $2,000 error. They have to wait until the total losses exceed $10,000. Some baskets are "tipping baskets" (where the seller pays everything once the limit is hit), while others are "true deductibles" (where the seller only pays the amount *above* the limit).

Then there are Survival Periods. Not all promises last forever. A "non-fundamental" representation-like a claim that all employee benefits are up to date-might only survive for 18 months after the deal closes. However, "fundamental representations," such as the fact that the seller actually owns the assets they are selling, typically survive much longer, sometimes even until the statute of limitations expires.

Who Controls the Defense?

When a third party sues, who gets to pick the lawyer? This is a huge point of contention because the person controlling the defense controls the strategy. If the indemnifying party controls the defense, they might want to settle quickly and cheaply, even if the settlement looks bad for the indemnified party's reputation.Usually, the party paying the bill (the indemnifier) wants the right to control the defense. However, the other party often insists on the right to "participate" by hiring their own lawyer at their own expense. If there is a conflict of interest-for example, if the seller is being sued along with the buyer-the buyer will typically have the right to take over the defense, provided the seller still pays the costs.

Common Pitfalls to Avoid in Generic Transactions

Many people treat indemnification as boilerplate text, but that's a dangerous move. A few common mistakes can turn a protective clause into a liability:- Ignoring Notification Timelines: Many contracts require you to notify the other party of a claim within a strict window (e.g., 30 days). If you wait too long, you might waive your right to be indemnified entirely.

- Vague Triggering Events: Using phrases like "any and all losses" is too broad for a seller and too vague for a buyer. Be specific about what constitutes a breach.

- Forgetting Insurance: An indemnification promise is only as good as the money behind it. If the indemnifying party goes bankrupt, the promise is worthless. This is why requiring the other party to maintain specific Commercial General Liability Insurance is a critical safety net.

- Overlooking Governing Law: Some jurisdictions view "hold harmless" and "indemnify" as the same thing, while others treat them as distinct legal doctrines. Always ensure the governing law section of your contract aligns with your indemnification goals.

Structuring the Agreement for Different Roles

Your approach to these clauses should change depending on whether you are the buyer or the seller.If you're the Buyer, you want the widest possible scope. You want the survival periods to be long, the baskets to be low, and the caps to be high (or non-existent for fundamental breaches). You want to ensure that any "hotspot" issues discovered during due diligence-like a pending environmental lawsuit-are covered by a specific, negotiated indemnity that doesn't count toward the general cap.

If you're the Seller, your goal is to limit your "tail"-the amount of time and money you remain on the hook after the deal is done. You should push for a shorter survival period, a higher basket to filter out nuisance claims, and a strict cap on total liability. You should also try to limit indemnification to "actual losses" and explicitly exclude indirect or speculative damages.

What is the difference between a basket and a cap?

A basket is a minimum threshold of loss that must be reached before a party is required to start paying for indemnification. Think of it as a deductible. A cap is the maximum limit on the total amount one party is obligated to pay, regardless of how high the losses go.

Can a party be indemnified for their own negligence?

It depends on the language of the contract and local law. Some agreements allow for indemnification even if the indemnitee was partially at fault, but many jurisdictions forbid "broad-form" indemnification where a party is protected from their own gross negligence or willful misconduct.

How long do fundamental representations typically survive?

Fundamental representations-which cover things like company ownership, authority to sell, and tax status-usually survive much longer than general business reps. They often last for the entire duration of the applicable statute of limitations, sometimes several years after the transaction closes.

What happens if the indemnifying party doesn't have enough money?

This is a major risk in business transactions. To mitigate this, buyers often require the seller to maintain insurance or set aside a portion of the purchase price in an "escrow account" for a set period. If a claim arises, the money is paid from the escrow rather than trying to collect from the seller later.

Does "defend" always mean paying for lawyers?

Yes, in a legal context, the duty to defend requires the indemnifying party to manage and fund the legal defense of the other party against a third-party claim. This happens even if it later turns out that the claim was baseless.

Write a comment